Employer Resources

Free Benefits Analysis

We do the work, you see the benefits.

Your free benefits analysis will show you your options.

You're already paying for healthcare subsidies. Why not see if they can work for you?

Our entire business model is built on reducing as much of the time and cost to you as possible when it comes to providing benefits. So let us do the heavy lifting.

We'll present you with a free, zero-obligation opportunity analysis based on your business. If you have a group plan, we'll compare your new options to the plan you have now. We'll show you line-by-line what you can save, we'll show you how to increase your benefits, we'll explain the new regulations that may apply, and we'll even implement the new plan if you accept it (HR loves us).

We've also included a sample benefits analysis presented to a small business in Pflugerville, Texas.

How should I set my budget?

That's entirely up to you.

Every business is unique, and so is every budget. Depending on your needs, we will tailor a solution that fits.

What do you need to know about my business?

All we need are the basics.

Our goal is to give you the best picture possible of how much you can save while keeping your employees happy, insured, and productive.

What makes the most sense for your business -- and saves you the most -- may be a QSEHRA, an ICHRA, a traditional HRA, a group plan, simple stipends, refundable insurance, a combination, or none of the above. Letting us know your business size and the general makeup of your team (married or single, what type of coverage, etc.) gives us what we need to show you what your options are.

If you're not yet familiar with HRAs, check out our guide: What Is an HRA?

Do non-group plans really work? Are businesses doing this?

These plans absolutely work and small businesses across the United States are rapidly adopting the new model.

The HRA model has been 13 years in the making. It has been designed across 3 administrations and has involved the IRS, Congress, the HHS, and the DOL. It's stated goal is to lower the cost to small business owners of providing health insurance to their employees while promoting adoption of Marketplace plans. HRAs have bipartisan support and are growing rapidly among small businesses across the U.S.

Frankly, the two hurdles most small businesses face are simply (1) a lack of awareness and (2) the challenge involved in implementing something new. That's why we're here.

Can you show me an example?

We'd be glad to.

All data in the benefits analysis below (and subsequent employer plan) was taken from United Healthcare, the Marketplace, Globe Life Family Heritage Division, and the employees of a real small business in Pflugerville (only employee names have been altered).

Example Benefits Analysis

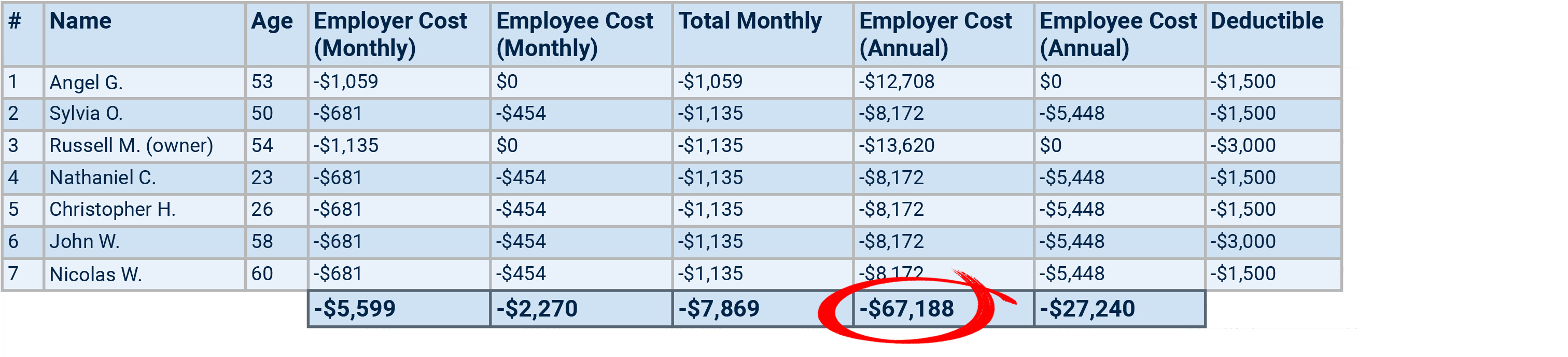

Part One - Original United Healthcare (UHC) Group Plan

Cost to Employer - $67,188/year

Cost to Employees - $27,240/year

The original UHC group plan included the owner and 6 employees. The business owner covered 60% of premiums and was facing a rate increase of 17%. Only a handful employees participated due to the high premiums. The total cost to the employer, including his plan, was more than $67,000 per year.

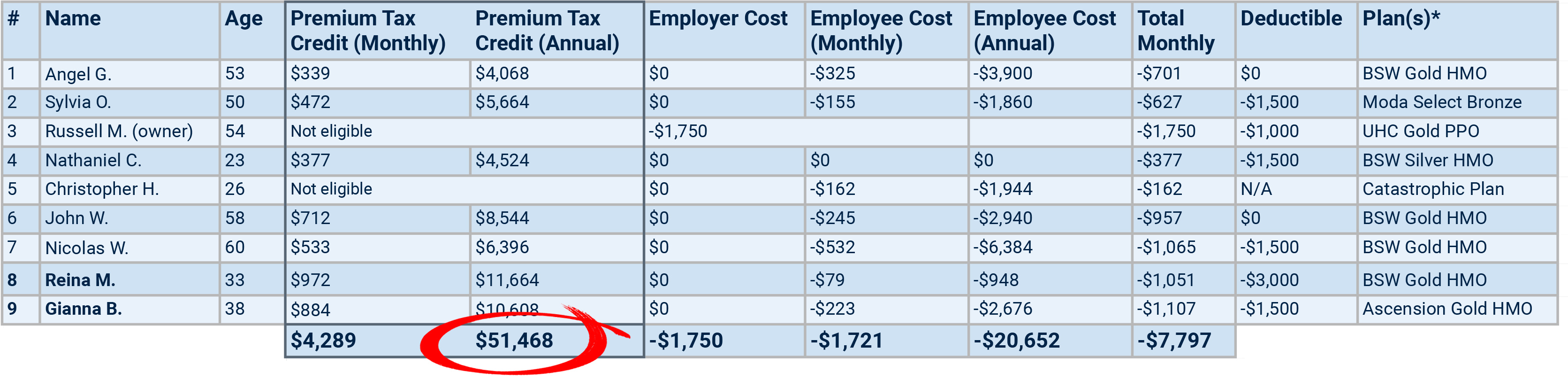

Our team provided him with a free benefits opportunity analysis, running his employees through the ACA and finding the total premium tax credits they were eligible to receive (below).

Part Two - Available Premium Tax Credits ($51,400/year)

Cost to Employer - $0/year

Cost to Employees - $20,652/year

Discovering that the ACA was ready to contribute $51,468 to his employees' health insurance was a game changer.

Using ACA gold plans as a guide, it was also clear that rates were going to decrease for his employees' share of the premiums when compared to the group plan. It didn't take long for the employer to see that this was a win-win.

Once we did, in fact, enroll his employees, rates decreased for the original group of covered employees, falling from $27,240 to $17,448 per year. Additionally, our benefits analysis resulted in two more employees being able to obtain affordable health insurance.* The final costs to all covered employees (9 total employees) came to $20,652 per year, still $8,748 lower than the employee share on the original group plan (7 total employees).

With the savings, the employer was able to substantially increase his employees' benefits overall, providing all 13 employees with refundable supplemental insurance policies through Family Heritage and adding a $50/month HRA to six employees.

*Employees are disqualified from Marketplace plans when an employer has a group plan in place that is considered "affordable". The employees originally waived the insurance due to the high monthly rates, but when they found they could get Marketplace plans at substantially lower rates, they were happy to start their new plans.

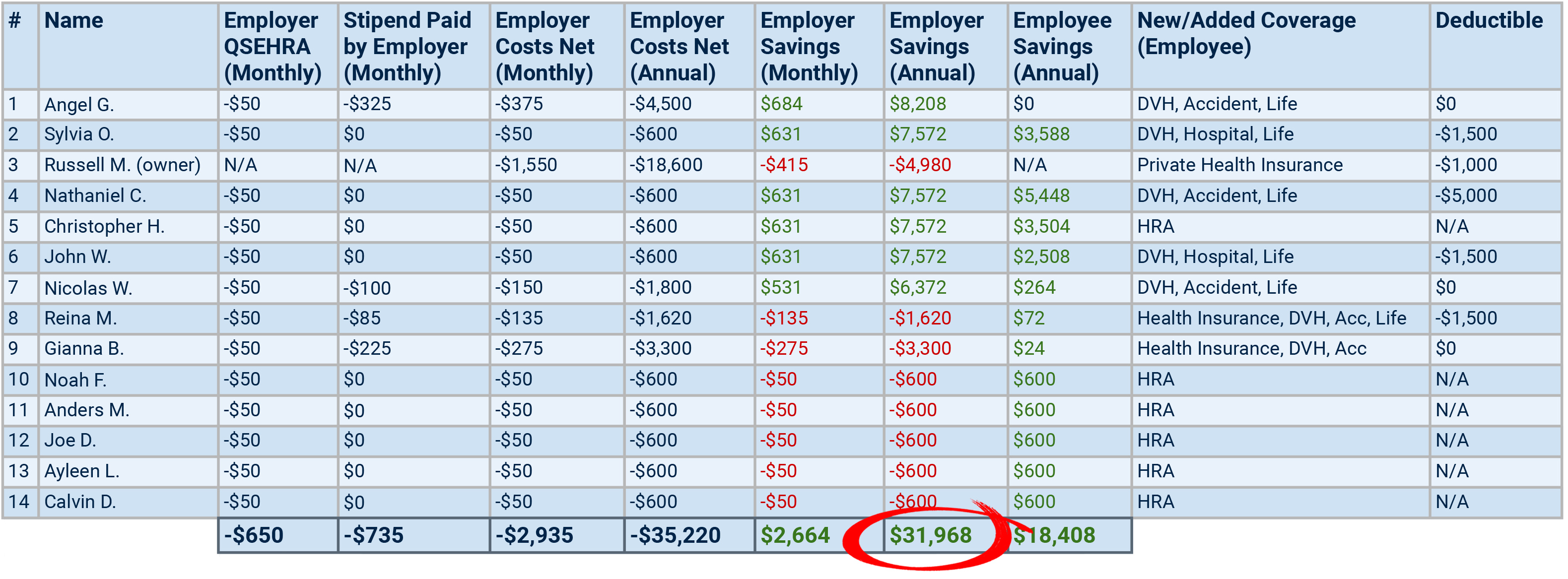

Our Recommended Benefits Plan

QSEHRA Plan Difference Table (Costs, Savings)

Savings to Employer - $31,968/year

Savings to Employees - $18,408/year

Not only did the employer save $31,968 per year on health insurance costs, but all employees combined saved $18,408 -- whether in lower health insurance premiums on plans they selected themselves or on new benefits through the HRA. Additionally, employees gained dental vision and hearing (DVH), accident, hospitalization, and life insurance coverage at lower costs to them than their original group plans.

Also note that the bulk of the employer's new costs are for his own private health insurance plan ($18,600 per year).

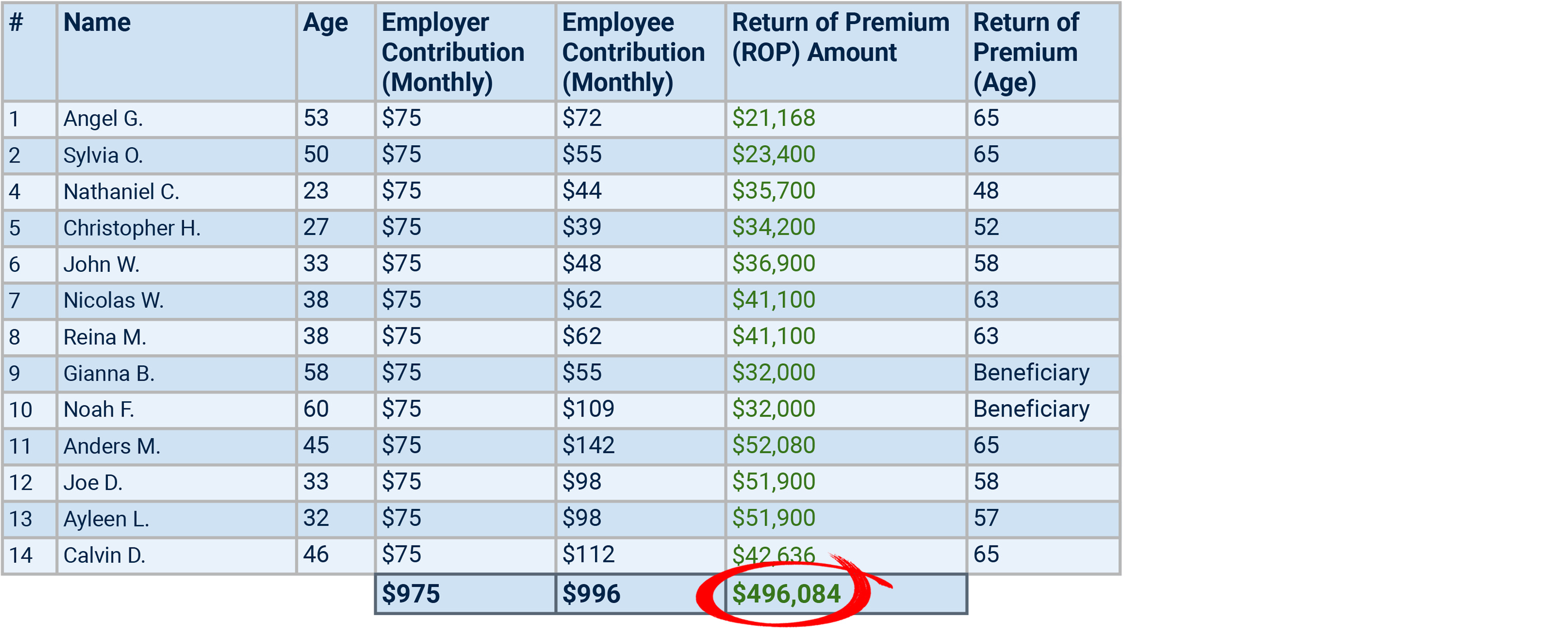

Additional Benefit - Family Heritage (Refundable Insurance)

Cost to Employer - $11,700/year

Potential Benefits Paid to Employees - Unlimited (no caps on claims)

Sayings to Employees - $496,084 (less claims)

Using a portion of the $31,968 per year savings, the employer supplemented his employees' benefits with Family Heritage refundable insurance policies. These policies will pay his employees unlimited supplemental benefits for covered health events and up to $496,084 in Return of Premium (ROP) savings.

Employees at this small business in Pflugerville can now boast better benefits than many large companies offer. Many of these employees have most, if not all, of the following: full health insurance coverage, dental vision and hearing, accident, hospitalization, a $50 HRA, employer-funded supplemental health insurance coverage, life insurance, and savings plans.

And the savings to the employer after the refundable insurance for all employees still amounted to $20,268.

Bring Uncle Sam to the table.

You've got nothing to lose by obtaining a free benefits opportunity analysis, but potentially much to gain.

See if premium tax credits and recent HRA legislation can help lower the cost of your health benefits, like they already are for thousands of other small businesses across the United States. If you do see a decrease in cost, you can use your savings to substantially improve the benefits your employees receive.

Once we've delivered your free plan summary, we will:

• Recommend a benefits plan for you that maximizes your available credits

• Work hand-in-hand with your employees to find them the best available plans

• Help you set up your HRA

• Expand your benefits (within your budget)

It takes less than 2 minutes to fill out our simple form and get the conversation started.

Our Process

1) You tell us about your business

2) We send you a free benefits analysis

3) We set up your plan

4) We enroll employees

Who We Serve

Employers (<50)

Employers (50-99)

Employees