Client Resources

Premium Tax Credits

If you own a small business and don't yet know what premium tax credits can do for you, you've come to the right place.

What are premium tax credits (PTCs)?

Premium tax credits are paid for by your tax dollars and show what the State stands ready to pay today for your employees' health insurance.

PTCs are subsidies created by the Affordable Care Act (ACA or "Obamacare") to make health insurance more affordable for Americans with moderate to lower incomes. Credit amounts are determined by age, family size, geographical location, access to health plans, and income. They are available immediately upon enrollment and can be used in full or in part to reduce employee monthly premiums.

In 2021, President Biden signed the American Rescue Plan Act which expanded eligibility for the subsidies. These enhanced tax credits are available to employees today.

Why am I reading about them now?

Because the opportunity for small businesses is relatively new.

In combination with other recent legislation -- specifically the 2016 Century Cures Act and a 2019 executive order

under the Trump administration -- small businesses have been able for just a few years now to provide health benefits while taking advantage of PTCs from the Marketplace. More employees than ever before are now eligible for subsidies.

Due to these changes, programs that allow small businesses to benefit from tax credits (HRAs, which we cover in the next question) have exploded in popularity. The only real barrier small business owners face to benefiting from the programs they already pay for is a simple lack of awareness. That's why we wrote this guide.

What can premium tax credits do for my business?

Premium tax credits can dramatically lower the cost of providing health benefits to your employees.

If you don't offer benefits because you think you can't afford it, there's a good chance this guide will change your mind. If you're offering a group health plan (GHP), then premium tax credits may be able to dramatically reduce the cost of your benefits.

Regardless of which group you're in, you will likely want to set up a Health Reimbursement Arrangement (HRA) such as a Qualified Small Business HRA (QSEHRA) or Individual Coverage HRA (ICHRA), but we'll cover those soon enough.

(To skip to learning more about HRAs, check out our QSEHRA Guide or take a look at our HRA Comparison Table.)

Are my employees eligible for premium tax credits?

The short answer is yes, they most likely are.

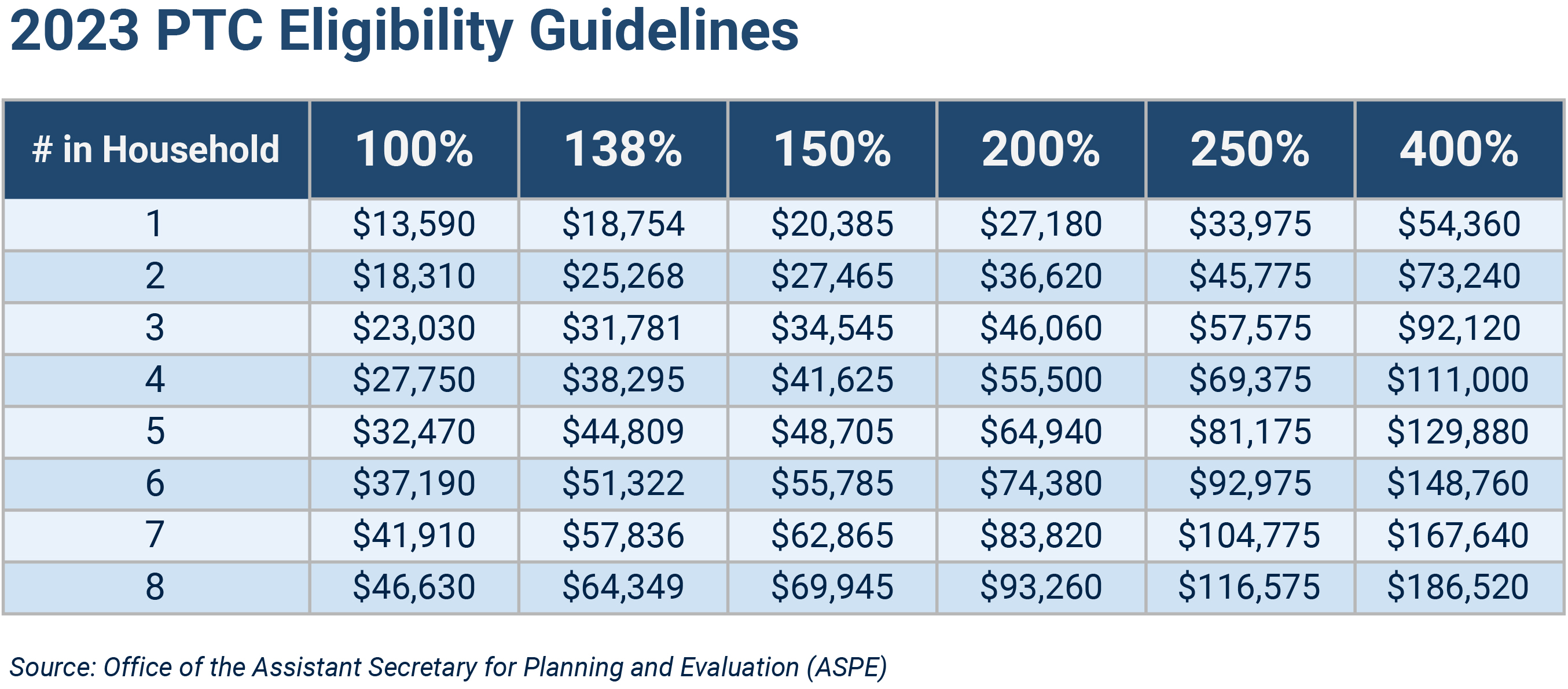

Anyone with an adjusted gross income (AGI) of up to 4x the federal poverty level is eligible for a premium tax credit. Below is a chart of employee eligibility based on income:

So I can still provide health benefits, but I can also take advantage of tax credits?

Yes. Small business owners are expressly allowed to benefit from the subsidies available to their employees on the Marketplace.

If you're thinking, "This seems like a game-changer" -- you're right.

HRAs have bipartisan support in Congress and are approved and regulated by the IRS, the HHS, and the DOL. More businesses are waking up every day to the realization that they can dramatically reduce the cost of benefits to their employees, or that -- perhaps for the first time -- they can afford to provide benefits to attract and retain the best employees.

Are HRAs good for just me or for my employees too?

HRAs are typically a win-win for small businesses, especially those with fewer than 50 employees.

Group health insurance lumps all employees into a one-size-fits-some plan -- giving employees little to no control over their coverage, network, deductible or premium amount. An HRA empowers employees to personally choose individual insurance plans that work for them. Each employee can use the benefit differently to cover the expenses that make sense for their personal health, budget, and family situation.

Employees very frequently see dramatic decreases in health insurance premiums, given the size of their available PTC. Employers get to reduce the cost of providing health benefits, gain control over how much they offer and to whom (whether in the form of an HRA or a simple stipend), and are finally freed from the headache of implementing and maintaining cumbersome and often overpriced group plans.

How much can my employees expect to receive in PTCs?

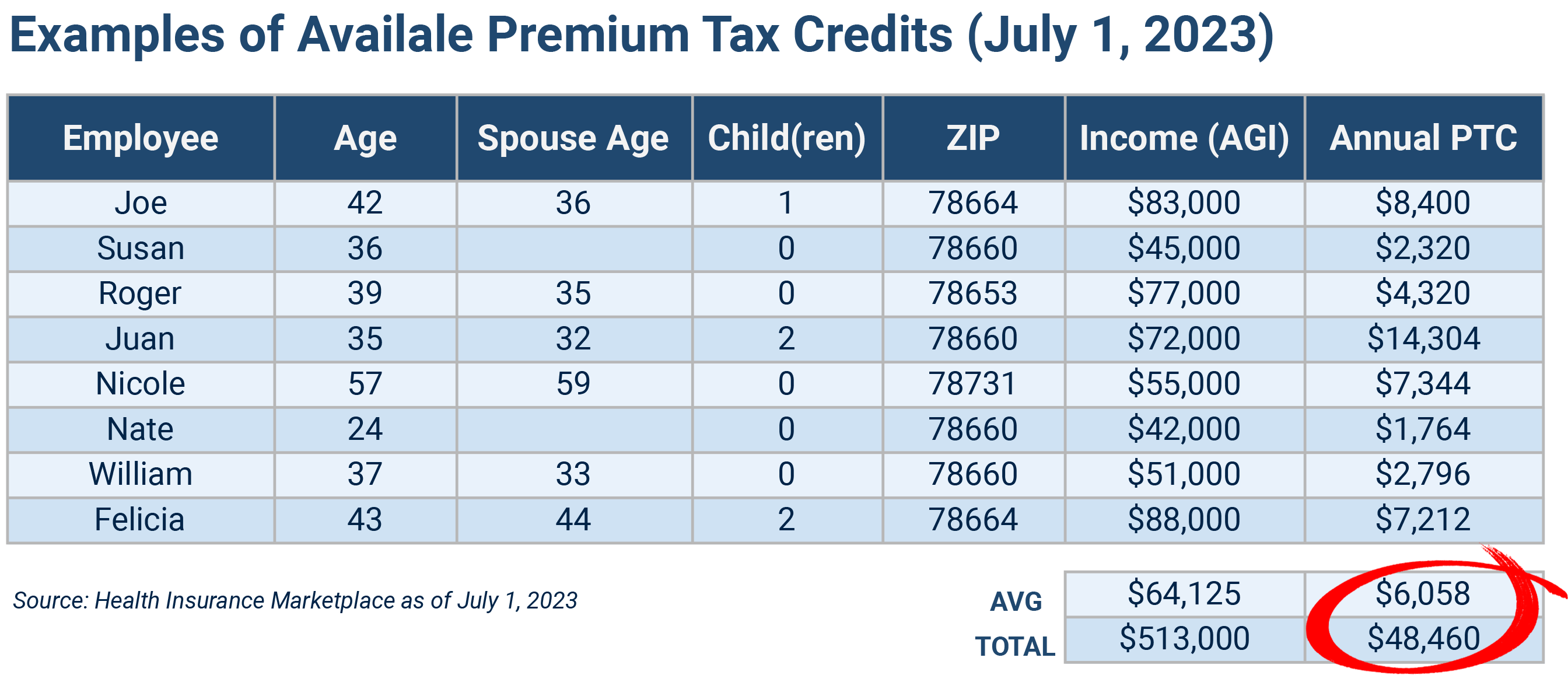

A typical employee in Texas earning $45,000-$75,000 can expect between $1,200 and $15,000 or more in premium tax credits per year.

The amount that employees are eligible to receive in premium tax credits varies based on income, family size, age, and residence (ZIP code). Here are some real tax credits available to employees from a business in Pflugerville, TX:

As you can see, the available tax credits are typically substantial.

HRAs allow you, the small business owner, to benefit from these subsidies while still offering healthcare benefits to your employees. To learn more about HRAs for small businesses, check out our QSEHRA Guide.

Does the premium tax credit work with any type of insurance?

PTCs are only available when employees choose plans from the Marketplace, healthcare.gov, or your state's insurance marketplace.

States like Texas have websites where employees can view and compare policies, receive their tax credits, and enroll in plans. A licensed health insurance agent is a great resource for help selecting a health plan (that's what we do!).

Are Marketplace plans just as good as other plans?

Yes, Marketplace, healthcare.gov, and state insurance marketplace plans are essentially the same plans.

Marketplace plans and non-Marketplace plans are typically mirror images of each other, though off-Marketplace plans don’t provide premium subsidies and enrollees will have to pay rate increases themselves. This means that people who don’t receive PTCs will generally pay less by picking lower-cost off-Marketplace health insurance on a private website.

How do I coordinate an HRA with premium tax credits?

Typically, the HRA contributes towards an employee's premiums and reduces the PTC by the HRA amount.

Depending on the size of your business and the premium tax credits that your employees are eligible to receive, you may end up choosing an HRA, a health stipend, refundable insurance, a combination, or nothing at all.

If you do choose to offer an HRA, employees choose their own health plan and you will reimburse them for premiums and/or other qualifying medical expenses up to their monthly allowance (although you can also pay for their premiums from the HRA allowance directly).

With a qualified small employer HRA (QSEHRA), employees can keep their health coverage tax credit and participate in the QSEHRA. However, employees must reduce their subsidy by the amount of their QSEHRA allowance, and they don't have the option to opt-out.

If you choose to offer an individual coverage HRA (ICHRA), your employees must choose between the ICHRA or their premium tax credits. They can waive their subsidy altogether if their ICHRA is considered "affordable." If it's not considered affordable, they can opt out of the ICHRA and continue collecting their PTCs.

To learn more about affordability and why it's important to you, see the answer to "What does affordability mean when it comes to my HRA?" in our QSHERA Guide.

To learn more about the different types of small business HRAs and how they compare to group plans, check out our complete table on GHPs vs ICHRAs and QSEHRAs.

How do I get started? What's the next step?

All we need is some basic information about your business and we will provide you with a free benefits analysis.

We'll gather together the total premium tax credits your employees are eligible for, we'll include a list of available plan options form the Marketplace, we'll compare those costs to your existing costs (or expectations), and we'll recommend an HRA allowance that maximizes the total PTC balance available in order to get your monthly cost of benefits as low as possible under the regulatory guidelines.

If you're currently offering a GHP, then our summary will give you a great idea of what you could save with an HRA. If you're providing benefits for the first time, then we'll show you what your options look like with an HRA vs a traditional group plan.

Fill out the form by clicking "Get Started" and schedule a quick call with our experts today. You'll be glad you took the the 2 minutes.

Our Process

1) You tell us about your business

2) We send you a free benefits analysis

3) We set up your plan

4) We enroll employees

Who We Serve

Employers (<50)

Employers (50-99)

Employees