Employer Resources

GHP vs ICHRA vs QSEHRA

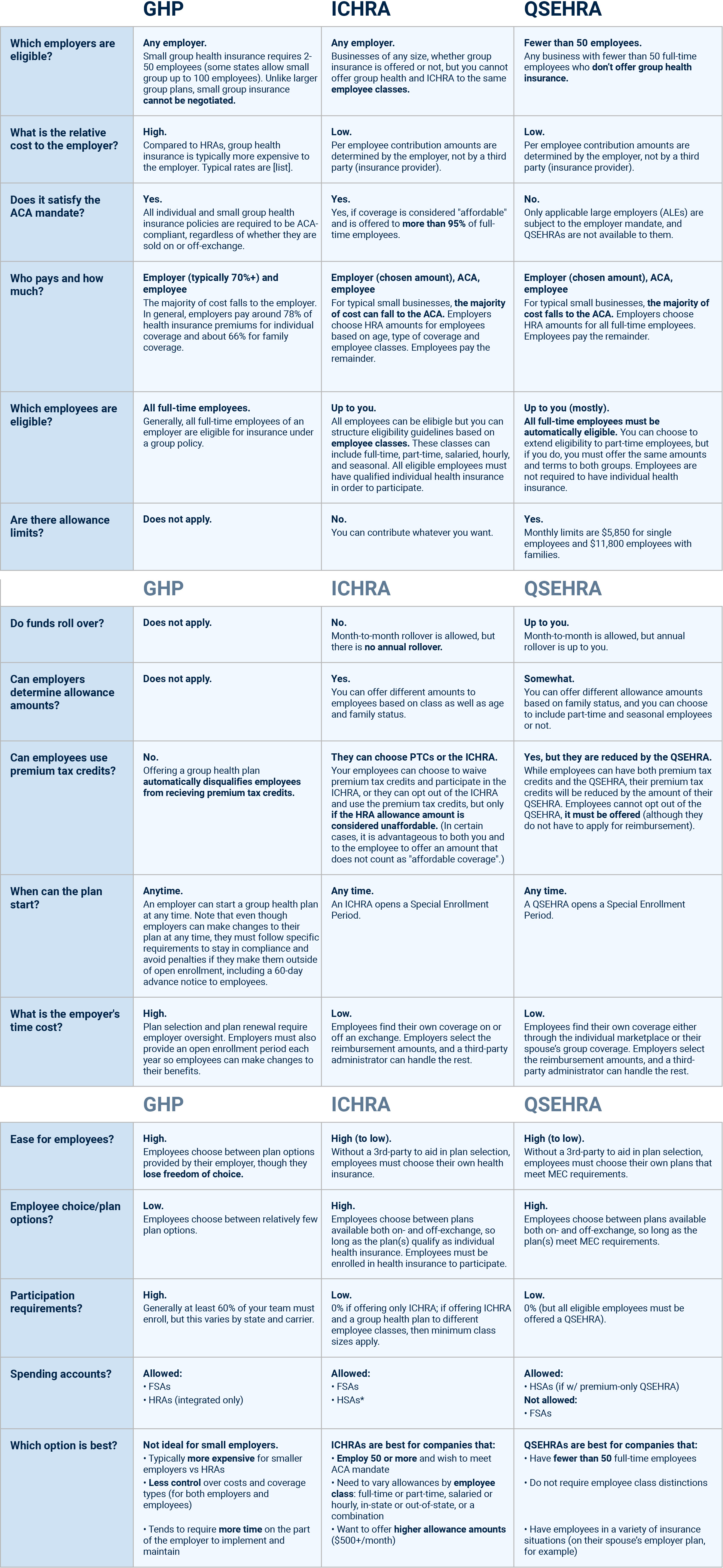

Discover which plan best fits your business.

What are the main differences between group health plans and HRAs?

The short answer for businesses with <50 employees is that HRAs allow you to benefit from premium tax credits from the Marketplace.

For larger businesses, HRAs (health reimbursement arrangements) can be used to help you control your costs, offer your employees greater choice when deciding on health insurance and to afford you greater control over the level of benefits you provide to different classes of employees.

If your business has fewer than 50 full-time employees and you are not yet familiar with premium tax credits (PTCs), the qualified employer health reimbursement arrangement (QSEHRA) or the individual coverage health reimbursement arrangement (ICHRA), then click on the corresponding links to learn more. To compare traditional group plans with HRAs, see the complete comparison guide below (note that this form is best viewed from a desktop).

Which HRA is right for me?

Generally, QSEHRAs are a better fit for businesses employing fewer than 50 people, with two exceptions.

QSEHRAs are limited to businesses employing fewer than 50 full-time or full-time equivalent (FTE) employees. HRA amounts per employee are capped at $450 per month for individual coverage, and $920 per month for families (limits will increase in 2023 to $490 and $980). Therefore, if you're an applicable large employer (ALE), you'll need an ICHRA.

QSEHRAs must be offered on the same terms to all full-time and FTE employees. Employers may choose to include part-time employees, but the QSEHRA must be offered to them at the same terms as well.

If you're not an ALE, you may still need an ICHRA if:

1) You're planning on contributing more than the monthly/annual QSEHRA limits

2) You want to contribute different amounts per employee class (hourly, salaried, full-time, part-time, seasonal)

It can get tricky, but don't worry. We've created a guide that lays out everything you need to know. We've also put together a simple 2-minute quiz that will tell you which HRA is right for you!

*This is only if the employee has individual insurance not purchased through an exchange, and the ICHRA needs to be reimbursing only premiums and not medical expenses, though employees can fund the HSA simultaneously. Otherwise, if employees want to use the ICHRA and HSA for premium and medical-expense reimbursements at the same time, the employee needs to be on a high-deductible health plan, the employer can't offer a group health plan to other employees, and the ICHRA needs to be set up in a way where additional conditions are met and restrictions apply.

I still have questions...

Great! We've got answers.

Take less than 2 minutes to fill out our simple form and get the conversation started.

Our Process

1) You tell us about your business

2) We send you a free benefits analysis

3) We set up your plan

4) We enroll employees

Who We Serve

Employers (<50)

Employers (50-99)

Employees